The Latest Labor Market Data is About to Appear

- Treasury yields are mostly unchanged this morning with a deluge of corporate debt issuance aided and abetted by sovereign auctions that are weighing on the fixed income market. Longer-dated debt is also confronting the issue of a Fed about to cut in the face of inflation that looks to be sticky at best, if not setting up for another leg higher. While the week is filled with data, today we’re left with a July JOLTS report that will begin to tell the latest labor/employment story that will finish on Friday with the BLS Nonfarm Payrolls Report for August. Currently, the 10yr Treasury is yielding 4.27%, down 1bp on the day, while the 2yr note yields 3.65%, also down 1bp in early trading.

- With the summer holidays officially over, the calendar immediately returns to work with a boatload of data set to fill this holiday-shortened week. Friday’s August employment report headlines the data, and while results aren’t likely to alter the expected September rate cut it could start setting the stage for the pace of cuts that may come after.

- As for jobs, expectations are for another month of mediocre job gains. Headline growth is expected to be 80 thousand new jobs, 75 thousand private jobs, with the unemployment rate increasing a tenth from 4.2% to 4.3%. Just as important as those two numbers will be, will be the revisions to the prior two months that last month cut a whopping 258 thousand jobs from initial estimates.

- Fed Governor Christopher Waller, in a speech last week, detailed the trouble with the jobs report and the reduced level of survey responses that have hindered initial estimates. What Waller explained is that companies have three months to submit their payroll surveys and initial reporting has been getting later, meaning companies are eventually submitting their surveys but at a slower pace than had been typical pre-pandemic. Thus, that leaves the initial estimates from the BLS subject to larger errors. As those late surveys arrive that’s when the revisions begin.

- There’s also the question of the birth/death model that has been overestimating new company creation, and hence jobs, since the pandemic and while the BLS has been adjusting this model, it is still contributing to an over-estimate of job creation that is being reversed in later months as actual data starts to arrive. Suffice it to say, the report will give us plenty to talk about when it arrives on Friday.

- Before then we’ll get the July Job Openings and Labor Turnover Survey tomorrow. Job openings have been trending lower and that will be the focus tomorrow. While job openings are continuing to decrease the Quits Rate remains near 2.0% level which is at the pre-pandemic range which speaks to workers feeling less optimistic about the labor market and that is a sentiment that has been obvious in other consumer surveys.

- Tomorrow also brings the ADP Employment Change Report that had been given little respect in the last year or so when it failed be anywhere close to the initial BLS numbers, but with the huge revisions from the BLS, the ADP report should get renewed respect this week. Last month, ADP reported 104 thousand private sector jobs when the BLS reported 83 thousand, and that’s prior to revisions that will be coming this Friday. A low print from ADP will only add to market angst of a slowing labor market.

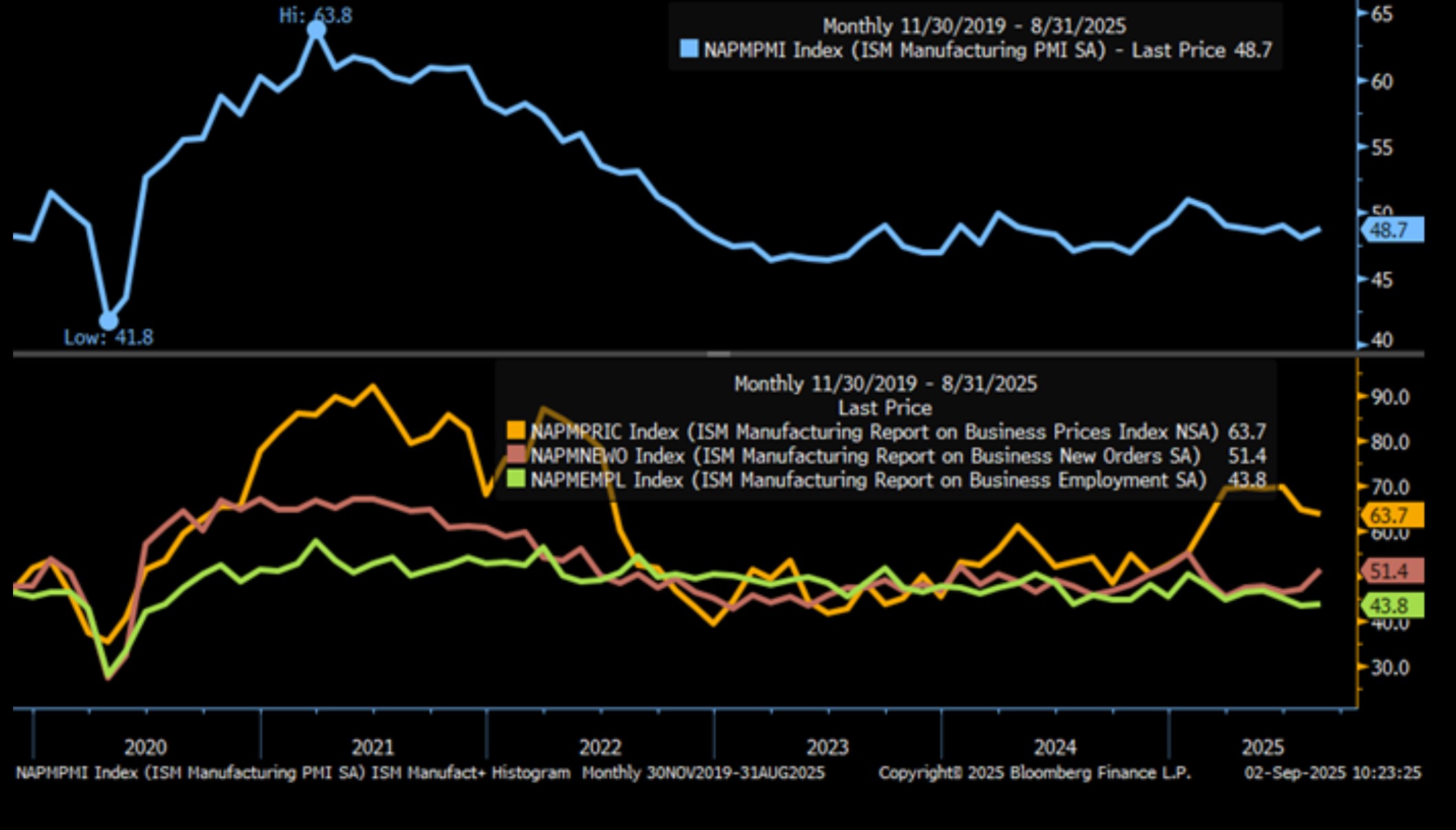

- The ISM Manufacturing Index for August was released yesterday with the headline measure improving slightly to 48.7% vs. 48% in July. While it’s slightly better activity the sector remains in contraction with sub-50 readings. The New Orders Index indicated growth in August following a six-month period of contraction; the figure of 51.4% is 4.3 percentage points higher than the 47.1% recorded in July and the first print above 50 since January. The Prices Paid Index remained in ‘increasing’ territory, registering 63.7% compared to 64.8% in July. The Employment Index improved to 43.8%, up 0.4 percentage point from July’s figure of 43.4%, but still well below the 50-level. Thus, not much improvement in the sector overall. Activity improved by the slightest of amounts, with new orders registering a nice bump, but prices paid remained high and employment showed little improvement.

- A review of respondent comments again focuses on the tariff issue and the uncertainty and difficulty in planning around policies that change daily; thus, the safest corporate thing to do is very little to nothing. That seems to be the popular response. So, don’t go looking for that manufacturing renaissance spurred on by tariffs anytime soon.

- The services side of the economy will get its ISM report for August tomorrow with a slight improvement from 50.1 to 50.5, but that’s still dangerously close to contractionary territory. As in the manufacturing sector, the employment, prices paid, and new orders indices will give us a decent assessment of whether the service sector is continuing to slow, as has been the case in recent consumer spending data, or if it’s a pause before the rebound.

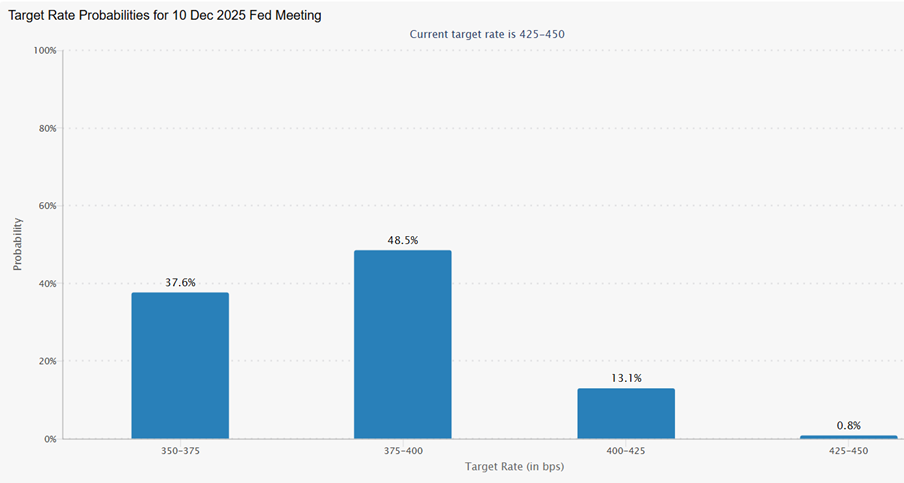

Fed Funds Futures See 50bps in Cuts by Year-End with Outside Shot at 75bps

Source: CME

30-Year Treasury Yield Approaching 5.00% – Are the Bond Vigilantes Stirring Again?

Source: CNBC

August ISM Manufacturing Index – Don’t Look for this Sector to Boost the Economy Anytime Soon

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.