July Jobs Report Reveals Acceleration in Labor Market Softening

July Jobs Report Reveals Acceleration in Labor Market Softening

- Nonfarm payroll gains for July were 114 thousand vs. 175 thousand expected and 179 thousand in June (revised down from an initial 206 thousand). May was revised lower by 2 thousand jobs, bringing the two-month revisions to -29 thousand and that continues a year-long trend of downward revisions, some rather substantial. The gain in July jobs was well under the 12-month average of 215 thousand. Meanwhile, private sector jobs increased 97 thousand vs. 141 thousand expected and 125 thousand in June (revised down from an initial 136 thousand). It’s the weakest private sector job growth since March 2023.

- In a departure from recent trends, the Household Survey (which generates the unemployment rate, labor force participation, etc.) reported a similar picture as the Establishment Survey. For July, the Household Survey reported an increase of 67 thousand jobs and saw an increase of 352 thousand in the ranks of the unemployed.

- Job gains were strongest in healthcare/social assistance (64k), leisure/hospitality (23k), construction (25k), and government (17k). Job losses occurred in information services (-20k), and for a fourth straight month temporary help services shed jobs, this time 8.7 thousand. This continuing trend signals softening in demand with firms reducing temp help first before moving to cut full-time workers.

- Average Hourly Earnings rose 0.2%, missing the 0.3% expectation which was the gain in June. The year-over-year pace decreased to 3.6%, missing the 3.7% expectations and down from 3.8% in June. Average weekly hours ticked lower to 34.2 hours, the first move lower since January. Weekly hours peaked at 35.0 a year ago and seems to be settling in the low 34-hour range, another sign of moderating labor demand.

- The moderation in wage gains, however, is what the Fed wants to see as it diminishes the potential for wage-price spirals. Ideally, the Fed wants that YoY number to drift down to 3.5%, or less, just above the 2% inflation benchmark, and thus providing some real (net of inflation) wage gains. Monthly prints in the 0.2% – 0.3% range do the trick.

- After two months of one-tenth increases, the unemployment rate rose two-tenths to 4.3% (4.252% unrounded), missing the 4.1% expectation, and 1% above the 3.3% low. The Household Survey reported an increase of 352 thousand in the ranks of the unemployed but also an increase of 420 thousand in the labor force. While increases in the unemployed stemming from a growing labor force are less problematic to policymakers, the number of unemployed persons has increased 1.25 million over the last year.

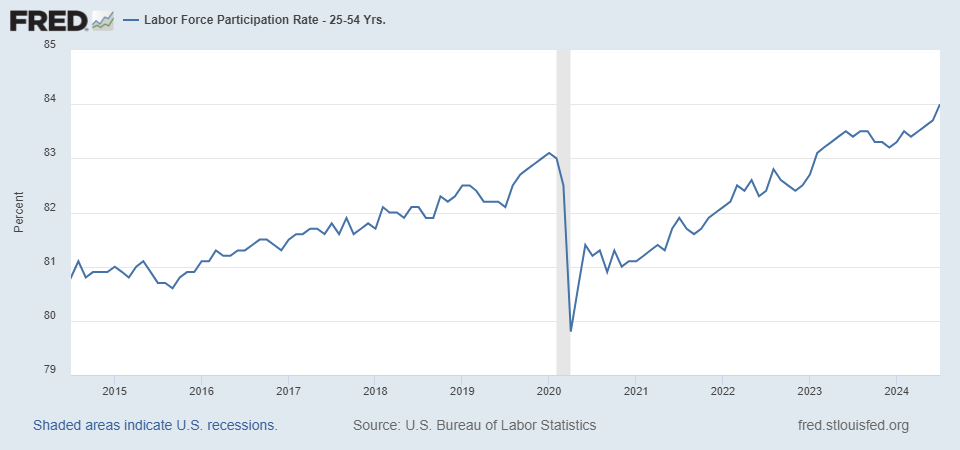

- As one would expect, the increase in the labor force led to an increase in the Labor Force Participation Rate of one-tenth to 62.7% beating the 62.6% expectation. The participation rate a decade prior to the pandemic ranged between 62.5% and 63.0% while the average over the past year has been 62.6%. The prime age (25-54yr old) group saw the participation rate increase from 83.7% to 84.0%, the highest post-pandemic rate and the highest in 24 years (see graph below). The somewhat stalled nature of the overall participation rate is more a function of the older cohort (>55yrs) leaving the labor force in increasingly larger numbers. Call it the revenge of the Boomers.

- After the June employment report noted some softening in momentum, July’s report clearly indicates the softening in the labor market is accelerating. Job gains are clearly slowing as the three-month average has dipped from 242 thousand a year ago to 170 thousand now and that includes a 216 thousand print in May, so clearly the average is poised to move lower. Wage gain moderation continued in July and while welcome news at the Fed it is another indication of easing in labor demand. Job losses in temporary help services continued for a fourth straight month, a clear sign of softening demand. This report is consistent with other recent labor-related reports that reflect a slowing in labor demand. The question to be answered is does the softening accelerate to the point that the Fed will be forced to cut 50bp in September? The futures market is already pricing that move in.

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.