February Jobs Report – Something for Everyone

February Jobs Report – Something for Everyone

- Nonfarm payroll gains for February were 275 thousand vs. 200 thousand expected and 229 thousand in January (revised down from an initial 353 thousand). In fact, the prior two-months were revised lower by 167 thousand jobs which continues a year-long trend of downward revisions. Private sector jobs increased 223 thousand vs. 160 thousand expected and 177 thousand in January (revised down from an initial 317 thousand). Recall, APD reported 140 thousand private sector jobs, coming in below the BLS figure once again. Of course, we’ll have to wait on next month’s revisions before casting judgment on ADP.

- Yet again, the Household Survey (which generates the unemployment rate, etc.)reported a much different number on jobs. In January the survey reported a loss of 31 thousand jobs and for February job losses totaled 184 thousand. Combined with the consistently large revisions to the Establishment Survey, and the ongoing volatility in the Household Survey, it does give one pause as to how much to conclude definitively from these BLS report.

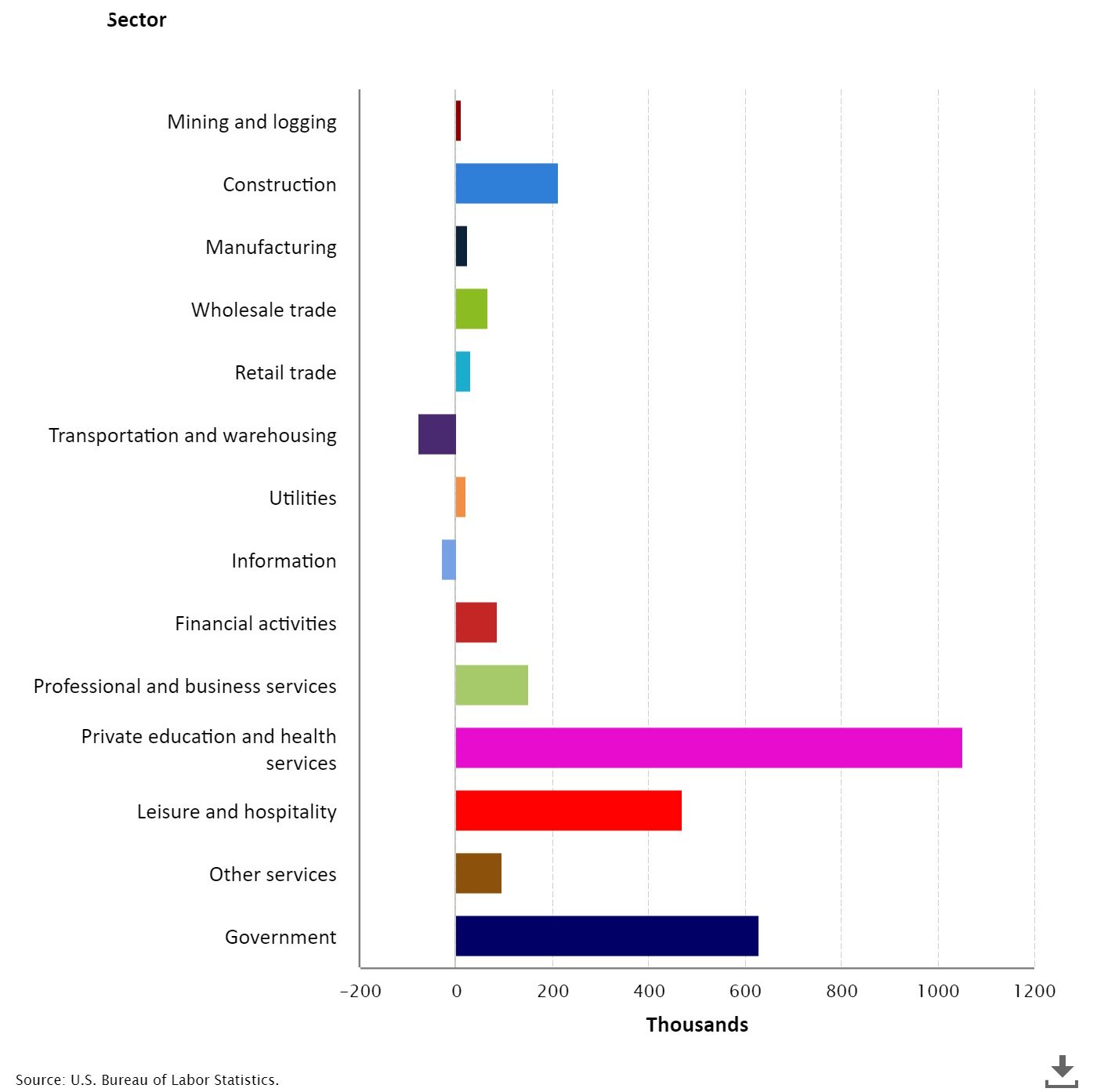

- Job gains were notable in healthcare (91k), leisure and hospitality (58k), government sector (52k), and transportation/warehousing (20k). Job losses were concentrated in temporary help services at 15 thousand, a sign of the decent breadth of job gains.

- Wage gains moderated after a strong January with a MoM gain of 0.1% vs. 0.3% expected and 0.6% in January. In addition, the year-over-year pace decreased to an as expected 4.3% vs. 4.5% in January. Average weekly hours increased 0.1 hours to 34.3 hours, matching the expectation. Weekly hours peaked at 35.0 a year ago, and it seems they are settling in that low 34 hour range, certainly not a sign of increasing labor demand.

- In addition, the moderation in wage gains is exactly what the Fed wants to see in order to tamp down the potential for a wage-price spiral. Ideally, the Fed wants that YoY number to drift to around 3.5%, or less, just above the 2% inflation benchmark. So, monthly prints in the 0.1% – 0.3% range will eventually do the trick.

- The unemployment rate rose two-tenths to 3.9%, above the expected 3.7% as the Household Survey reported an increase of 337 thousand in the ranks of the unemployed with a modest increase of 150 thousand in the labor force (the denominator in the unemployment rate calculation). That small labor force gain halts declines over the last two months.

- The increase in the ranks of the unemployed and small increase in the labor force as per the Household Survey kept the Labor Force Participation Rate unchanged at 62.5%, just under the 62.6% expectation. The participation rate a decade prior to the pandemic averaged 63.3% while the average over the past year has been 62.6%.

- All-in-all, this report has a little for everyone. While the topline job gains easily beat expectations, the moderation in wage gains and increase in the unemployment rate diminishes some of the potential heat of the headline beat. The Fed will like the slowing wage gains, but the unemployment rate popping two-tenths higher will have them moving forward some in their chairs. And with downward revisions likely, the job gains may turn out to be less than the robust number printed today. This so-so report will keep a June rate cut on the table, but CPI next week will have a bigger say in that matter.

Employment Change by Industry, 12 Months Seasonally Adjusted

Source: Bloomberg

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.