Cracks Slowly Appearing in Pockets of the Economy

- While we don’t have a BLS Nonfarm Payrolls Report today we will have the preliminary University of Michigan Sentiment Survey for November. Excited? Well, me neither. Also, while the Supreme Court hearing didn’t go particularly well for the Trump administration, it will most likely be a few weeks before a decision is handed down, and even if the ruling goes against the government, they have other paths to pursue tariffs, so this issue will be an ongoing matter regardless of the court decision. So much for policy clarity! Currently, the 10yr Treasury is yielding 4.09%, unchanged on the day, while the 2yr note yields 3.55%, down 2bps in early trading.

- The AI revolution may be enjoying the largess of investors looking to cash in on the latest tech innovation, not to mention the infrastructure build, it has also contributed to the most job cuts for any October in more than two decades, outplacement firm Challenger, Gray & Christmas reported. The last time companies made more layoffs during October was in 2003. 153,074 cuts were announced in October which is 183% above September’s and 175% above October 2024. Year to date, this is the worst year for layoffs since 2009, when the country was suffering through the Great Financial Crisis. The tech sector led the cuts with 33 thousand, that’s six times the September level. Yet, weekly jobless claims have yet to show a spike from the 220 thousand (ish) level of claims that has been the trend for many months. Often, laid off workers are given severance packages that can delay the filing of claims so there is that, but also with the government shutdown it complicates data collection and analysis, certainly across the whole of the US.

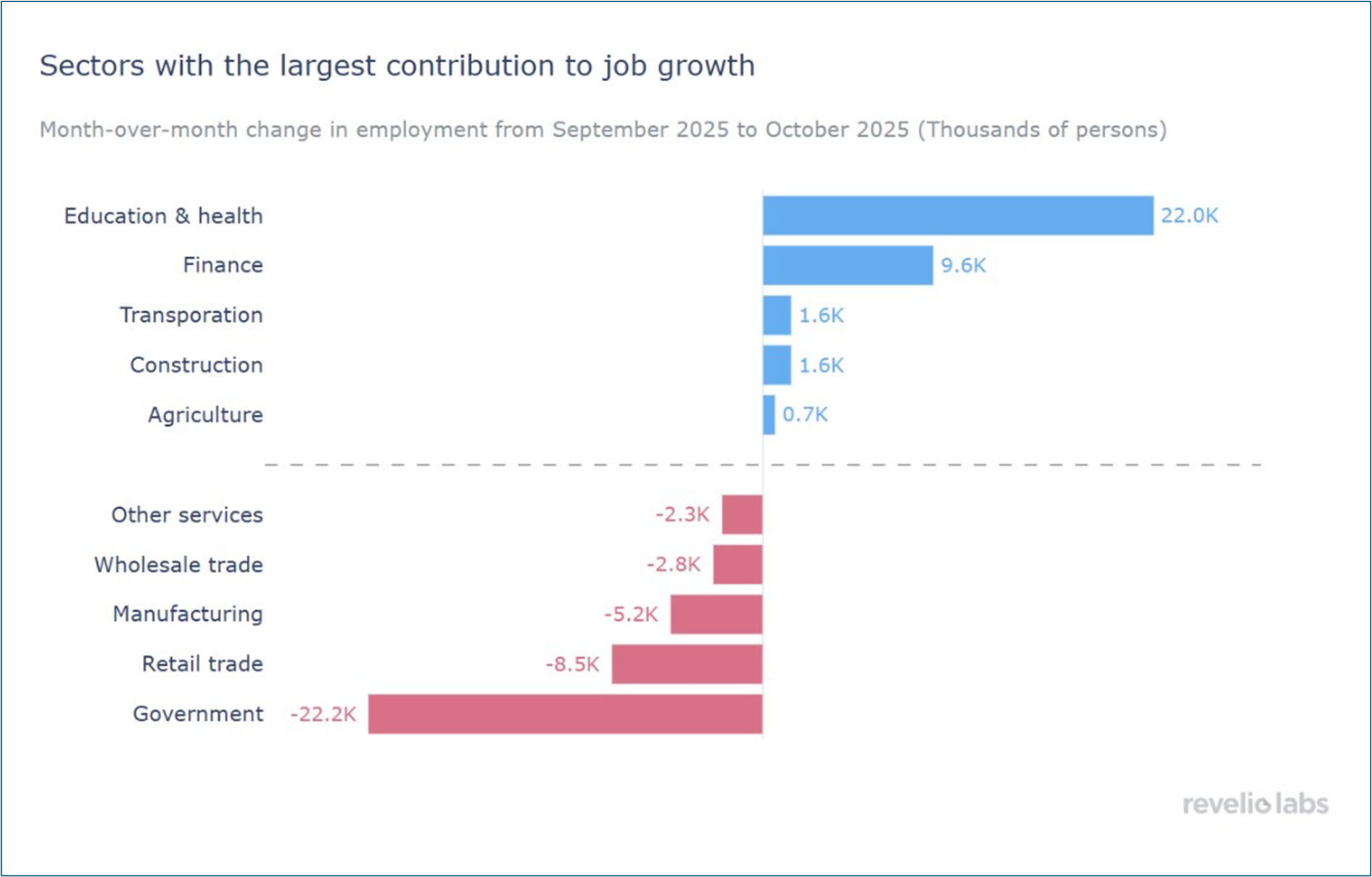

- Given we’re without an official jobs report we do have other providers stepping into the breach. In addition to ADP, we have Revelio Public Labor Statistics (Revelio Labs) which yesterday released its estimate of job growth for October. In September, Revelio Labs reported 60k jobs – quite a difference from ADP’s September print of -32k (subsequently revised to -29K). For October, ADP reported 42k private sector jobs while Revelio Labs reported only 13k private sector jobs and a loss of -22k government jobs for a combined -9k jobs lost in October. Revelio reported job growth in Education and Health Services and weakness, no surprise, in the Government sector (see table below).

- Looking at Jan 2021 – July 2025 data, Revelio Labs data tracks the BLS Establishment Survey with a correlation coefficient of 0.74, a marginal improvement on ADP’s 0.70 figure. Given that, one can surmise the October ‘truth’ lies a touch closer to Revelio Labs. Admittedly, we’re grasping at statistical straws but it’s difficult to make a case that employment today remains ‘resilient’. Hiring growth is suppressed and the path forward remains as uncertain as ever, which doesn’t argue for any near-term improvement. No doubt, the push/pull between the dual mandates of price stability and full employment will continue to be a challenging path to navigate for the Fed as we finish the year and venture into 2026.

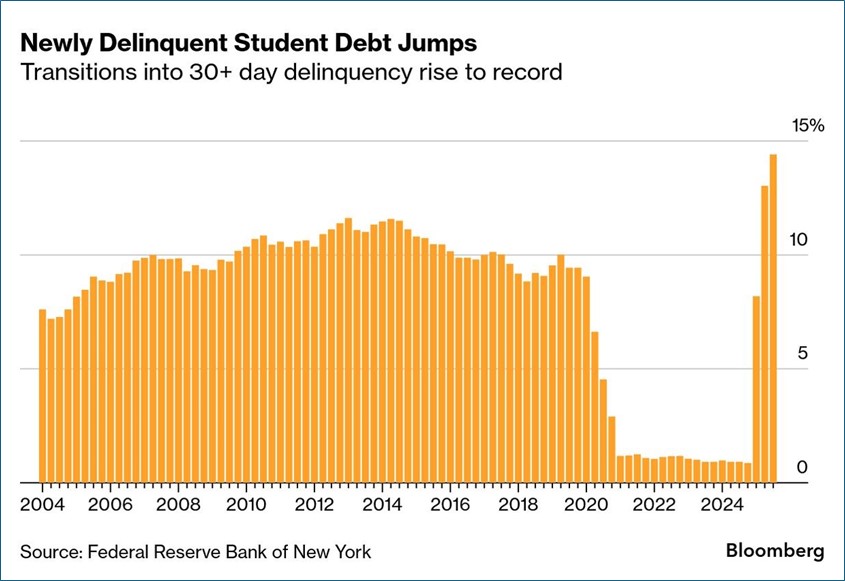

- Meanwhile, the share of US consumer debt in delinquency rose in the third quarter to the highest level in more than five years as unpaid student-loan balances continued to surge (see graph below). Around 4.5% of debt was at least 30 days delinquent in the July-to-September period, the most since the first quarter of 2020. The data comes from the Federal Reserve Bank of New York in its Quarterly Report on Household Debt and Credit. The share of student-loan debt becoming delinquent climbed to 14.4%, the most on record. The figures suggest US households — especially younger ones — continue to grapple with financial challenges resulting from high interest rates, weak hiring trends, and ongoing inflation. Transitions into serious delinquency were most elevated for consumers in their 20s and 30s, the report showed. Thus, the K-shaped economy rears its head yet again.

- And if right on cue, there were some positive signs in the report. While the share of student loans becoming seriously delinquent continued to rise, the overall amount in serious delinquency ticked lower after surging in the previous two quarters. The share of mortgage loans — the largest component of overall consumer debt — that was past due remained low. So, once again it’s a confusing picture where pockets of stress are noted but, on a macro basis it’s still not at concerning levels. Recall, at the October FOMC press conference Fed Chair Powell said he was “paying close attention” to credit conditions following recent reports of significant losses at sub-prime auto credit institutions, but added he didn’t see, “at this point, a broader credit issue”, and that seems to be the case here. There are pockets of concern for sure, but so far, no indication it’s spreading deeper across the economy.

- We didn’t get a chance yet to opine on the ISM Services Index for October, which was released late Wednesday morning. It was a touch better than expected, but with concerning price increases that helped drive yields higher after its release. The headline number rose from 50.0 to 52.4, beating the 50.8 expectation. The prices paid component rose again to 70.0 vs. 69.4 in September which caused consternation in the Treasury market while employment rose to 48.2 vs. 47.2 in September and beating the 47.6 expected. New orders also overachieved at 56.2 vs. 50.4 in September. The pop in new orders and prices paid components will nag at Fed officials wanting to continue cutting rates while it will give fuel to the hawkish members wanting to wait until better inflation numbers arrive, and this report did not deliver that.

- At 10am ET this morning we’ll get the preliminary November University of Michigan Sentiment Survey. Expectations are sentiment will slip slightly to 53.0 vs. 53.6, while Current Conditions improve ever-so-slightly from 58.6 to 58.9 and Expectations remain unchanged at 50.3. Inflation expectations over the next year are also expected to be unchanged from October at 4.6% and longer-term inflation (5-10yrs) is expected to improve slightly to 3.8% vs. 3.9% the prior month.

- Last call! At last week’s Elevate Bank Forum, I sat down with Dr. Elliot Eisenberg, one of our guest speakers at the conference, where we talked about the economy and his outlook for 2026. He’s quite the entertaining guy in the field of economics so give this 20-minute discussion a listen. The link is here.

Revelio Labs – Monthly Change in Jobs by Sector

Source: Revelio Labs

ADP – Wage Gains by Geographic Area

Student Loan Debt – With Interest Payment Deferments Ended Delinquencies Increase

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.