August CPI was OK, Greenlighting a Rate Cut Next Week

- Treasury yields are ticking higher this morning with little to drive them as most of the known event risk for the week has passed, and eyes now turn to next Wednesday’s FOMC rate decision. The CPI report yesterday, while not great, was good enough to green light a rate cut, but truth be told the focus is now more on how weak the labor market has become while the Fed has sat in pause mode so far this year. The last data point due this week is of the survey variety with the 10am ET release of the Univ of Michigan preliminary Sentiment Survey for September. That won’t be a game changer, so we set sights on next week’s FOMC event. Currently, the 10yr is yielding 4.07%, up 5bps, while the 2yr is yielding 3.56%, up 4bps on the day.

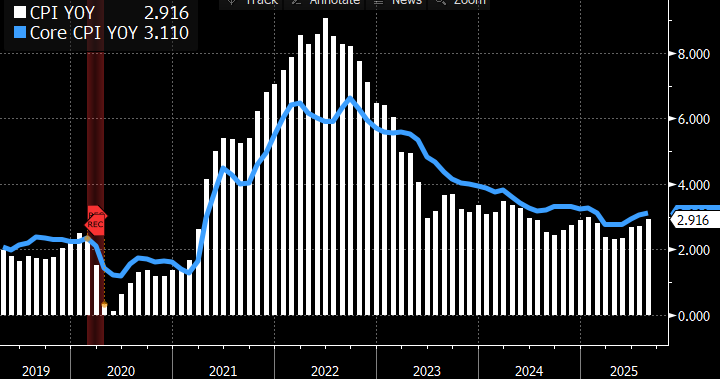

- The August CPI report was greeted as close enough for government work and that provided the final grease to the skids for a rate cut next week, and probably a couple more before year end. We did note, however, a few nagging issues in the results that will cause some of the Fed inflation hawks to squirm a bit if the trend persists. First, core services ex-housing continues to be uncomfortably high, albeit less than the unexpected surge in July. Recall, this is the ”sticky” component of inflation that Powell has focused on while waiting for Owner’s Equivalent Rent (OER) to roll over. While core services did print at 0.33% MoM vs. 0.48% in July, that remains the third highest this year and nearly 4.0% annually. The “stickiness” of this non-tariff sector will remain an area of concern.

- Speaking of OER, it printed at 0.38% (0.4% rounded) after a more docile 0.28% print in July and is the second highest this year. After July’s result, hopes were that this single largest piece of CPI (27% weighting) was back within the 0.20% – 0.30% range that prevailed pre-covid. It looks, however, like this metric will remain a monthly uncertainty despite current rental measures drifting lower. Thus, don’t expect OER to bail out higher goods and service prices anytime soon.

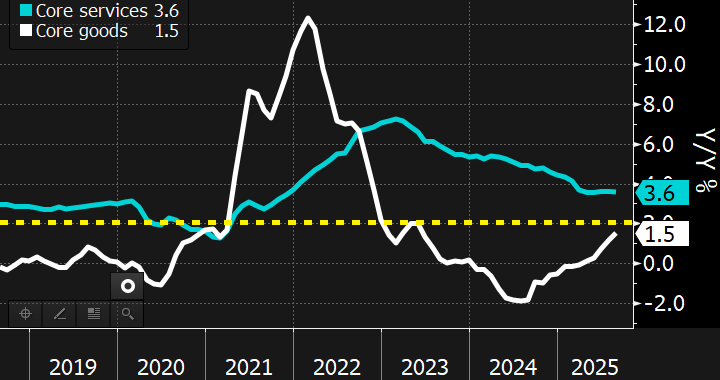

- Also, core goods prices, popped in August to 0.41%MoM vs. 0.07%MoM in July revealing that tariff costs are increasingly seeping into goods prices. Recall this sector was generally deflating in 2024 but that price action flipped in January and is adding to the service side inflation pressure instead of moderating it like it did last year. (see the YoY graph below). The consumer is likely to continue to see higher goods prices in the months ahead, especially as those wholesalers currently absorbing tariff costs eventually relent and pass those costs on.

- Looking ahead, it’s hard to see where lower prices are going to come from as goods prices lift along with services. In addition, 72% of CPI items have annual rates greater than 2%, the highest percentage since August 2022. That speaks to the broadening of pricing pressure. While a slowing economy will dent consumer demand and presumably limit retailers’ ability to pass through higher prices, that is weak soup to see that stagflation may be the out for higher prices. Thus, like last month, we continue to see 0.3% MoM core CPI prints over the balance of the year and that means YoY levels in the 3% – 3.6% range.

- Thus, the inflation numbers alone don’t argue for three rate cuts by year-end, but the limited move in prices, combined with the rapid softening in the jobs market, does argue for a more aggressive rate-cutting posture to support the full employment mandate.

- Meanwhile, the other shoe we’ve been watching in the labor market may have just dropped last week. Initial jobless claims for the week ended Sept. 6 jumped 27 thousand from 236 thousand to 263 thousand. That’s the highest claims total since October 2021 and perhaps a signal that employers are no longer content to limit new hiring but are now moving more aggressively to reduce existing headcount. Jobless claims had been relatively static this year, but the fear has been if demand slowed enough employers would move to increase layoffs to offset softening demand amid increasing product costs.

- We can offer a couple caveats to that bleak observation and that is holiday weeks are often problematic in their seasoning adjustments, so with Labor Day last week that fits the bill. Also, Texas saw a jump in claims to 32 thousand (vs. 16.6 thousand the prior week and apparently related to flood-related claims filing), so that may be a one-time jump. Anyway, trying to explain away a bad number is always risky business, so we’ll just say one week does not a trend make. That said, given all the issues recently with BLS’s nonfarm payroll estimates the weekly jobless claims data will be a key release for market watchers for the next several months.

- Later this morning, the preliminary Univ. of Michigan Sentiment Survey for September will be released. Expectations are that sentiment was relatively unchanged at 58.0 vs. 58.2 in August with Current Conditions and Expectations improving a bit from the prior month. More importantly, the 1Yr inflation outlook is expected to be nearly unchanged at 4.7%, with 5-10Yr inflation outlook a bit softer at 3.4% vs. 3.5% in August. While these inflation outlooks have risen in recent months, along with the Conference Board’s inflation surveys, the Fed has recently taken to speaking only about “market-based measures” like TIPS inflation breakeven rates as being “well anchored”. We imagine the Fed would like these consumer expectations to cool further so they can speak more confidently about anchored expectations.

August CPI Met Expectations, but Improvement is Non-Existent

Source: BLS

Core Goods Prices Moving Higher While Core Services Has Stopped Trending Lower

Source: BLS

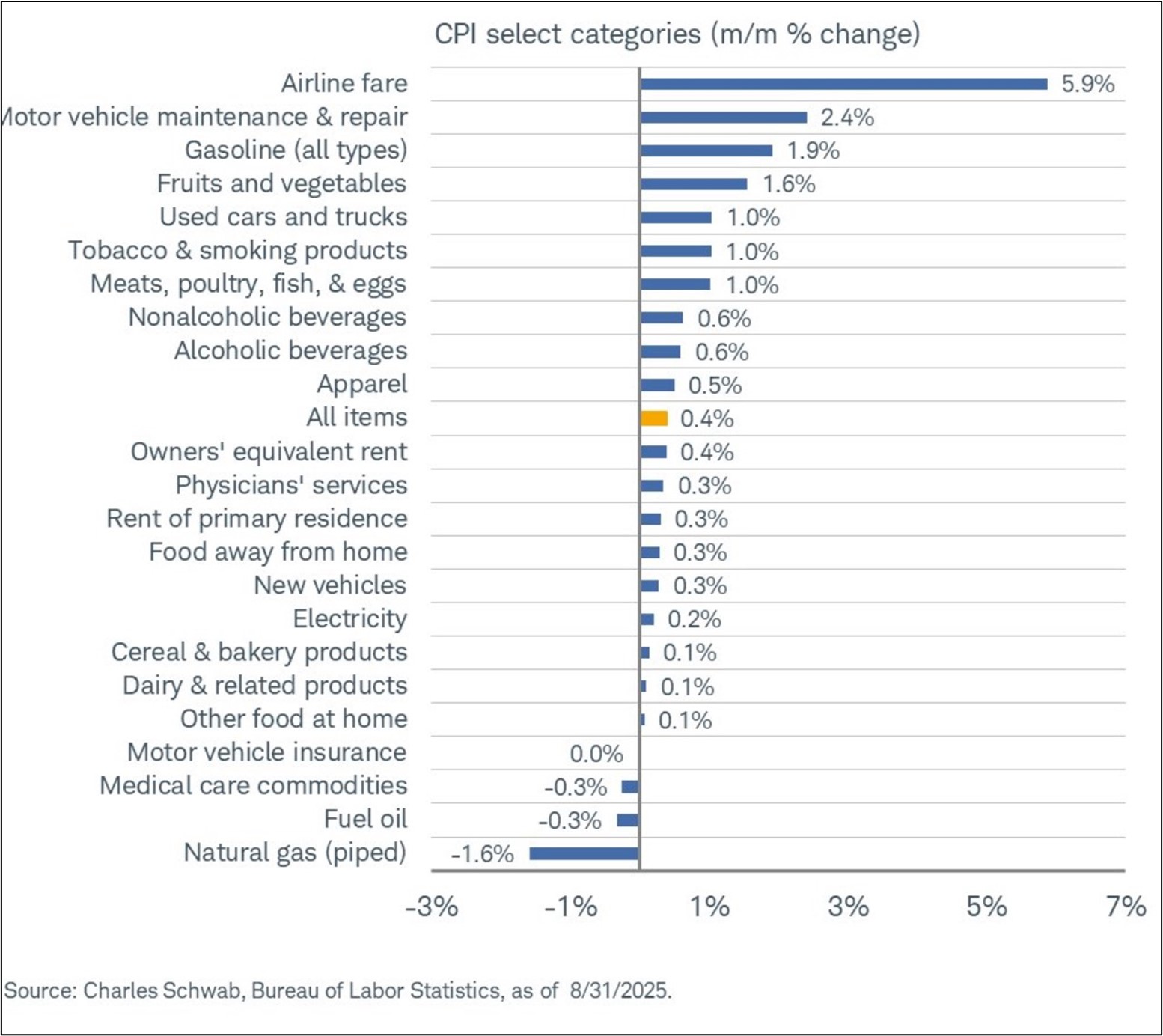

Another Good Month for the Airlines

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.