Are Consumers Finally Starting to Buckle Under Higher Rates?

Are Consumers Finally Starting to Buckle Under Higher Rates?

- Treasuries are drifting around unchanged as investors ready for the weekend. Fed speak yesterday was pretty much on script as to higher-for-longer and policy is in a good place for the time being. A couple more Fed officials (Williams and Daly) go today but one is a commencement address and the other on payment innovation so we don’t expect any policy headlines. The only economic report left for this week is the all but discredited Leading Indicators Index which has been flashing recession warnings for over a year to no avail, so expect it to come and go without much impact. Currently, the 10yr note is yielding 4.40%, up 2bps and the 2yr is yielding 4.80%, up 1bp.

- Inflation Week was successfully navigated, more or less, and while the reports didn’t signal an all-clear on inflation they did show some modest improvement and that was enough for most investors. One more inflation report arrived yesterday that did indicate another tailwind from 2023 has turned into a headwind. Import prices for April rose 0.9% vs. 0.3% expected and 0.4% in March. Import prices ex-petroleum rose 0.7% vs. 0.1% expected and 0.0% the prior month. The YoY rate increased from 0.4% to 1.1%.

- Last year, we were consistently importing deflation and now that story is over. The good news is that while we run a multi-billion dollar trade deficit, and import prices edging higher, its impact on overall price levels in a $20 trillion economy will be limited. On the export side, prices rose 0.5% vs. 0.2% expected and 0.3% in March. On a YoY basis, export prices are slowly moving up from -1.4% in March to -1.0%. So, while still in deflationary territory that impulse is fading as well. This is price pressure at the margin, to be sure, but it does add another complication to getting down to the Fed’s 2% inflation target.

- Meanwhile, April housing starts rose from 1.321 million annualized to 1.36 million but was short of the 1.42 million expectation. Meanwhile, housing permits slowed from 1.467 million to 1.440 million which was short of the 1.480 million expected. The question with this report is the softening solely a function of higher mortgage rates, a reflection of softening consumer demand, or both? One month does not make a trend but it does increase our desire to search for more canaries in the coal mine regarding the health of the consumer.

- Meanwhile, weekly jobless claims came in close to expectations at 222 thousand new claims vs. 220 thousand expected and below the multi-month high of 231 thousand the prior week. The claims figures have had an uncanny tendency to reside in the low 200 thousand range this year so the pop to 231 thousand last week got some anxious that the hint of job softening in the April employment report was repeating itself in May. Well, maybe it is but it doesn’t seem like it will happen in a straight line.

- While much was made of the soft retail sales numbers we offered up the caveat that it followed a strong March and it’s a much more goods-focused report, and as we all know the consumer has been more service-focused for a while. We will add too that one of our favorite real-time indicators, the TSA Security Screening Statistics, is still showing airline boardings consistently ahead of last year, which was equal to or better than 2019 pre-pandemic levels. So, for travelers, both leisure and business, the beat goes on.

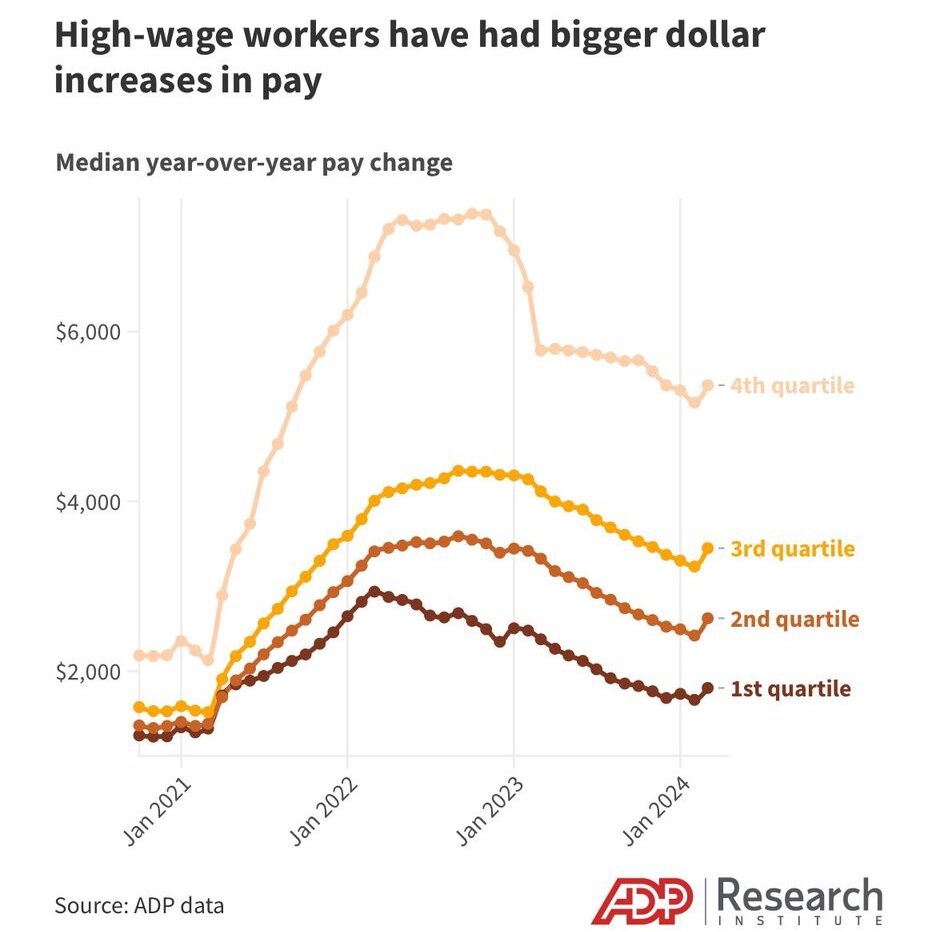

- The graph below, courtesy of ADP, shows most of the wage gains concentrated in the upper quartile of earners. That makes sense, so perhaps we’re starting to see a bifurcated market where lower income consumers are feeling the weight of higher rates and cutting back on discretionary spending, while those more well-heeled are still feeling quite comfortable. The May 31 Personal Income and Spending Report for April will provide a more comprehensive look at spending, not to mention the PCE inflation series, so suffice it to say it will be a focus for investors and the Fed before we turn the calendar to June.

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.