2nd Quarter GDP Precedes FOMC Announcement

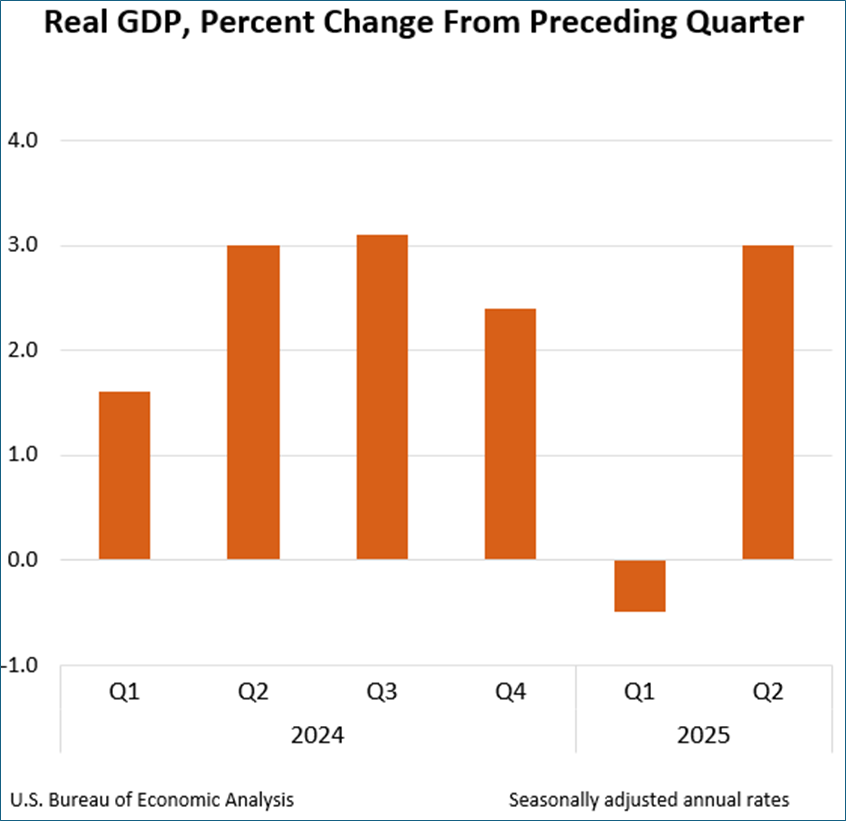

- Treasury yields are trading a bit higher after this morning’s new data headlined by 2nd Quarter GDP coming in at 3.0% beating most estimates, but with some nagging questions. A reversal of the 1st quarter import surge led to the rebound. As we march through the thicket of first-tier data on offer this week, the market remains somewhat tentative until clear of this afternoon’s FOMC announcement and press conference. We talk more about what to expect below. Currently, the 10yr Treasury is yielding 4.37%, up 4bps on the day, while the 2yr note yields 3.92%, also up 4bps in early trading.

- The FOMC concludes its two-day meeting this afternoon with what’s widely expected to be no change in rates. With no updates to the dot plot and economic projections, the only information on offer will be the post-meeting statement and Powell’s press conference. The presser will be the highlight, but we suspect that while Powell will surely be questioned about Trump’s characterizations of his job performance and unwillingness to cut rates at the moment, he’s enough of a DC veteran at this point to deftly deflect away those questions without creating controversy. While eyes are fixed on the September meeting for a possible cut, we also suspect Powell will defer to the inflation and jobs data that will be on offer between now and then. In summary, we expect a placeholder meeting today with Powell not tipping his hand yet about September.

- In the midst of the Fed meeting, a boatload of first-tier data is greeting markets with the first estimate of second quarter GDP the highlight for today but make no mistake every day this week will provide a bevy of new data for investors and the Fed to ponder as odds of a September rate cut will be refined.

- Speaking of GDP, the initial estimate for the second quarter was 3.0%, beating the 2.5% expectation (but similar to the Atlanta Fed’s GDPNow 2.9% final estimate). The result was quite an improvement from the 1st quarter’s -0.5% decline when tariff front-running pulled in huge imports subtracting from GDP. That reversed in the second quarter with the slowdown in imports adding nearly 5% to GDP in the second quarter. Meanwhile, personal consumption improved from the 1st quarter’s mediocre 0.5% to 1.4%.

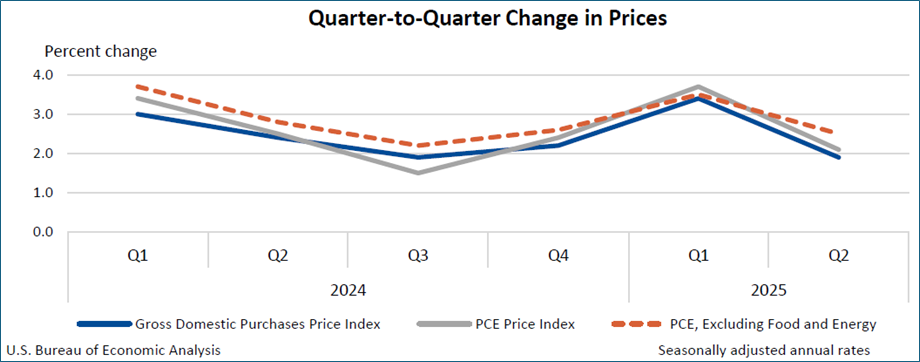

- We should note the Final Sales to Private Domestic Purchasers, which removes the volatile components like inventory, trade, and government spending, rose only 1.2% vs. 1.9% in the first quarter, the lowest since Q422. So, with all the volatility in the one-off items between the first and second quarter core consumption softened a bit in the second, something to keep in mind. Finally, the inflation series saw some good news with overall PCE increasing 2.1% QoQ annualized vs. 3.7% in the first quarter. Core PCE was 2.5% vs. first quarter’s 3.5% pace. So, net-net, better headline GDP growth coupled with cooler inflation but the softening in private sales to domestic purchasers warrants some consideration before declaring all is well.

- Payroll processor ADP is out with its Employment Change Report for July and reported a surprise 104 thousand new private sector jobs vs. 80 thousand expected and an upward revision to June from -33 thousand jobs lost to -23 thousand. We offer the usual caveat that ADP and BLS don’t often see eye-to-eye on the private payroll numbers so while the upside beat today may provide some revisions to Friday’s BLS expectation of 100 thousand jobs, it’s likely to be only on the margins. ADP’s chief economist characterized the monthly data as “broadly indicative of a healthy economy. Employers have grown more optimistic that consumers, the backbone of the economy, will remain resilient.” That was buttressed by the broad-based gains across labor categories and across varying sizes of firms. Annual pay gains were unchanged for July with Job-stayers received 4.4% gains and job-leavers saw 7.0% annual wage gains.

- The Treasury didn’t offer any real surprises in its latest quarterly funding needs announcement with coupon auction sizes expected to remain the same for the foreseeable future with any additional funding focused on T-bills to provide that capital. So, that soothes some nerves with those that thought coupon sizes might be in store for increased issuance but that was not the message today. Treasury Secretary understands the impact of long-term rates on mortgage rates so he’s not about to shift the mix when lower longer-term rates are wanted.

- From yesterday, the Conference Board reported improved consumer sentiment to 97.2 vs. 96.0 expected and 95.2 in June. The labor differential however (jobs easy to find minus jobs hard to get) fell to 11.3 , the lowest since March 2021. Stephanie Guichard, Senior Economist, characterized their findings with this, “consumer confidence has stabilized since May, rebounding from April’s plunge, but remains below last year’s heady levels. In July, pessimism about the future receded somewhat, leading to a slight improvement in overall confidence. All three components of the Expectation Index improved, with consumers feeling less pessimistic about future business conditions and employment, and more optimistic about future income. Meanwhile, consumers’ assessment of the present situation was little changed. They were a tad more positive about current business conditions in July than in June. However, their appraisal of current job availability weakened for the seventh consecutive month, reaching its lowest level since March 2021. Notably, 18.9% of consumers indicated that jobs were hard to get in July, up from 14.5% in January.”

- We’ll be back in the afternoon with a review of the FOMC rate decision and any comments that come from the Powell press conference.

GDP Rebounds on Reversal of 1st Quarter Import Surge

Reversal of First Quarter Import Surge Leads to 2nd Quarter GDP Pop

Inflation Levels Improved from 1st Quarter Giving the Fed Another Reason to Consider a Cut, but not Today

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.